Every Little Thing You Ought To Know About House Mortgages

Article writer-Atkins JorgensenIs it time to get a mortgage, or do you need to wait? What kind of mortgage can you afford? What company do you choose? Your mind is probably full of questions, and this article is going to help you with some answers. After all, choosing a mortgage is a major decision in which you want to be informed.

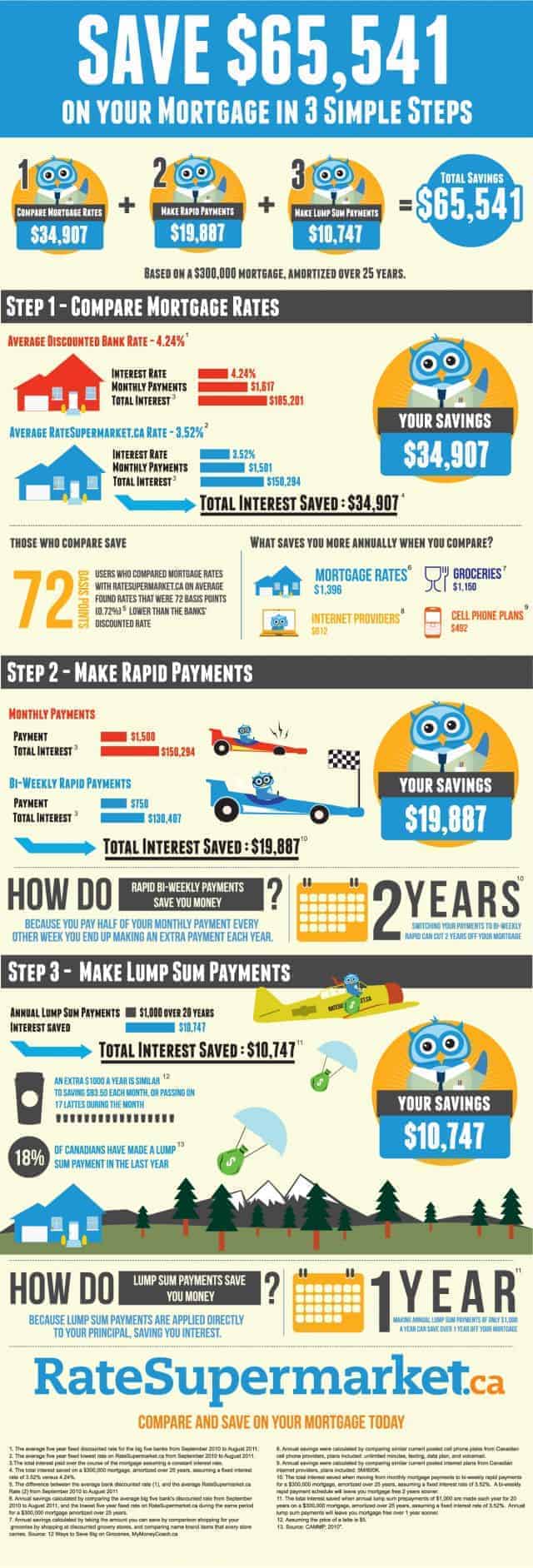

To make sure that you get the best rate on your mortgage, examine your credit rating report carefully. Lenders will make you an offer based on your credit score, so if there are any problems on your credit report, make sure to resolve them before you shop for a mortgage.

Prepare for the home mortgage process well in advance. Buying a home is a long-term goal that requires tending to your personal finances immediately. This means you need to save up a decent sized nest egg, and make sure your debt is well situated. If you put these things off too long, you could face a denial letter.

Getting the right mortgage for your needs is not just a matter of comparing mortgage interest rates. When looking at offers from different lending institutions you must also consider fees, points and closing costs. Compare all of these factors from at least three different lenders before you decide which mortgage is best for you.

Before applying for a mortgage loan, check your credit score and credit history. Any lender you visit will do this, and by checking on your credit before applying you can see the same information they will see. look at here now can then take the time to clean up any credit problems that might keep you from getting a loan.

When you see a loan with a low rate, be sure that you know how much the fees are. Usually, the lower the interest rate, the higher the points. These are fees that you have to pay out-of-pocket when you close your loan. So, be aware of that so you will not be caught be surprise.

You can request for the seller to pay for certain closing costs. For example, a seller can pay either a percentage of the closing cost or for certain services. Many times the seller is responsible for paying for a termite inspection along with a survey and appraisal of the property.

Be sure to check out multiple financial institutions before choosing one to be your mortgage lender. Look at their reputations on the Internet and through friends, and look over the contract to see if anything is amiss. When you have all the details. you can select the best one.

Speak with many lenders before selecting the one you want to borrow from. Know what these lenders are all about, and check with family and friends to get a good picture on what they will charge you. After you have all the information, you can make a smart choice.

Make sure you pay down any debts and avoid new ones while in the process of getting approved for a mortgage loan. Before a lender approves you for a mortgage, they evaluate your debt to income ratio. If your debt ratio is too high, the lender can offer you a lower mortgage or deny you a loan.

Be sure to compare the different term options that are available for home mortgages. You could choose between a number of options, including 10, 15 and 30 year options. The key is to determine what the final cost of your home will be after each term would be up, and from there whether or not you would be able to afford the mortgage each month for the most affordable option.

Knowledge is power. Watch home improvement shows, read homeowner nightmare types of news stories, and read books about fixing problems in houses. Arming yourself with knowledge can help you avoid signing a mortgage agreement for a house needing expensive repairs or an unexpected alligator removal. Knowing what you are getting into helps you avoid problems later.

Make sure you've got all of your paperwork in order before visiting your mortgage lender's office for your appointment. While logic would indicate that all you really need is proof of identification and income, they actually want to see everything pertaining to your finances going back for some time. Each lender is different, so ask in advance and be well prepared.

Pay your mortgage down faster to free up money for the future. Pay a little extra each month when you have some extra savings. When you pay the extra each month, make sure to let the bank know the over-payment is for the principal. https://www.natlawreview.com/article/dc-oag-reaches-4-million-settlement-fintech-over-claims-predatory-lending do not want them to put it towards the interest.

You need to be prepared to increase your down payment if your credit score is not up to par. A lot of new homeowners save about five percent of the value of their home but it is best to save up to twenty percent. You will be more likely to get a mortgage if you have more saved up for your down payment.

Before you even start looking at a new home to buy, try to get pre-approved for a home. This will give you confidence when looking for a new home and let you know what your budget is. It will also save you from choosing a home only to find out you cannot secure a large enough loan to purchase it.

Don't assume your bank is going to have the best mortgage for you. Sometimes lending companies will give you the better deal, so it's important to shop around. Definitely get an offer from your bank, too, but be open to going elsewhere. It can mean a lot of money in your pocket over the term of the loan.

Remember that interest rates are important, but they are not the only consideration. There could be other fees, depending on the bank. Consider the points, type of loan and closing costs being offered. You should get estimates from a few different banks before making a decision.

The ideas in this article have taught you the best practice when it comes to getting a mortgage. You have no reason to feel overwhelmed by the process now that you know how to get the job done right. Take your time, utilize each tip and turn your mortgage journey into a positive outcome.